Writer: Adam West

Editor: Lillian Guevara-Castro

Reviewer: Ashley Fricker

“How long after bankruptcy can I buy a house?” It’s a question we’ve heard more than once, and in this article, we’ll offer some valuable insight into this topic that impacts Americans all over the country. As children, many of us are taught — usually by our older siblings — to fear the monsters who hide under the bed. Of course, by the time we’re adults, we realize that the only monsters under the bed are the dust bunnies, busily multiplying like, well, bunnies.

Although we may outgrow the monsters under the bed, adults often have their own monsters to fear. For example, when it comes to our personal finances, the biggest, baddest monster of all is bankruptcy. And we’re not the only ones who fear bankruptcies — banks are afraid of them, too.

What’s more, that fear not only means you’ll be stuck with credit damage and poor rates, but it also likely means putting off your new home purchase as your bankruptcy “seasons” for at least a year, though the exact amount of time you’ll need to wait will depend on the type of bankruptcy you filed and the type of loan you’re seeking.

Let’s take a look at some valuable insights regarding bankruptcies and purchasing a new home, including information on conventional mortgages, FHA mortgages, and VA mortgages.

You May Need to Wait 4+ Years for a Conventional Loan

A conventional loan is any loan not backed by an outside agency — i.e., not FHA, VA, or USDA loans — but offered by a bank or non-bank lender. Because these loans are not secured against default by a third party, they present the highest risk to mortgage lenders.

As such, conventional mortgage loans tend to have the most rigorous qualification requirements, including the highest credit score and down payment requirements.

Along those same lines, conventional loans will typically have the longest seasoning requirement for bankruptcy discharges, requiring applicants to wait up to four years after bankruptcy to qualify for a loan. The rates you’re offered at this point may not be as good as if you were to wait for the bankruptcy to fall off your report, but comparison shopping, such as through an online lending network, may still reveal some interest-rate deals.

That four-year period may vary depending on the type of bankruptcy you filed. Under Fannie Mae, if you filed for Chapter 7 or Chapter 11 bankruptcy, you’ll need to wait at least four years unless you can prove extenuating circumstances.

In the event you can document that your bankruptcy was essentially out of your control, you may only need to wait two years before you can qualify for a conventional mortgage.

A two-year waiting period is permitted if extenuating circumstances can be documented, and is measured from the discharge or dismissal date of the bankruptcy action. — Fannie Mae

With Chapter 13 bankruptcies, the seasoning period will depend on whether your bankruptcy was discharged or completely dismissed. If your Chapter 13 bankruptcy was discharged, you’ll need to wait at least two years from the discharge date to qualify for a conventional mortgage.

If your Chapter 13 bankruptcy was dismissed, you’ll need to wait at least four years from the dismissal date.

For frequent filers, the time penalty is more severe. Those who have more than one bankruptcy filing within the past seven years will need to wait at least five years from the most recent dismissal or discharge date to become eligible for a conventional mortgage.

The exception here is if the most recent filing was for documented extenuating circumstances, which can cut the wait down to three years.

FHA Requires at Least 2 Years of “Seasoning”

As a loan backed by the Federal Housing Administration (FHA), FHA mortgage loans present lower risk to banks and lenders. This allows FHA mortgage lenders to offer more relaxed credit score and down payment requirements than can generally be found with conventional loans. And this extra leeway extends to the FHA’s bankruptcy seasoning requirements, which can be as little as a year.

Just as specific credit score and down payment requirements can vary by individual lender, however, the exact amount of time you’ll need to wait to qualify for an FHA loan may also be longer for certain lenders. Online lending networks can be an easy way to get quotes from multiple lenders with a single application, reducing the risk of falling short of one lender’s seasoning requirements.

The specific amount of time you’ll need to wait before applying for an FHA mortgage will be primarily dependent on the type of bankruptcy you filed. To get the one-year waiting period, you’ll need to have filed for Chapter 13 bankruptcy and made all of your payments on time for at least that one year. If you filed for Chapter 7 bankruptcy, you’ll need to wait at least two years before you’ll become eligible for an FHA loan.

Another government-backed mortgage option considered by those looking at properties in qualifying rural areas is a USDA-backed home loan supported by the Department of Agriculture. These loans can be an excellent option for those who qualify, as they don’t require any down payment, but you may need to meet minimum income requirements. Additionally, a recent bankruptcy will need to season for at least three years.

While the USDA places no minimum credit score requirements on mortgages, lenders may require a fair credit score of at least 620. If you currently lack safe rural housing and cannot qualify for any other loan, the USDA also offers the Section 502 Direct Loan Program. Section 502 loans have no down payment or minimum income requirements but are only for those who can demonstrate extreme need.

VA Loans Require a 1- to 2-Year Wait

Members of the various branches of the US military have difficult jobs — but somebody’s gotta do them. Given all they do for the country, it’s only fair that they get a little back now and then, and some of that comes in the form of the ability to use a VA-backed home loan to buy a house.

Mortgages backed by Veterans Affairs (VA) are low-risk for lenders, so they can often be obtained despite low credit scores and small (or nonexistent) down payments. Furthermore, VA-backed home loans have short bankruptcy seasoning waits, requiring as little as one year after filing to become eligible for a loan. You’ll need a certificate of eligibility to qualify for a VA loan, which can be obtained online.

As with other types of mortgages, the specific amount of time you’ll need to wait after a bankruptcy will depend on the type of bankruptcy you filed. The one-year wait applies to those who file for Chapter 13 bankruptcy, while those who file for Chapter 7 bankruptcy will need to wait at least two years before they’ll become eligible for a VA loan.

Bankruptcy Isn’t an End to Homeownership

For many children, the monster under the bed or in the closet is a very real threat, one that required making regular checks for such invaders a necessary part of the nightly routine. And although many of us eventually outgrow those childhood fears, adulthood quickly replaces them with new fears — ones that can’t be dispelled simply by turning on the bedroom lights.

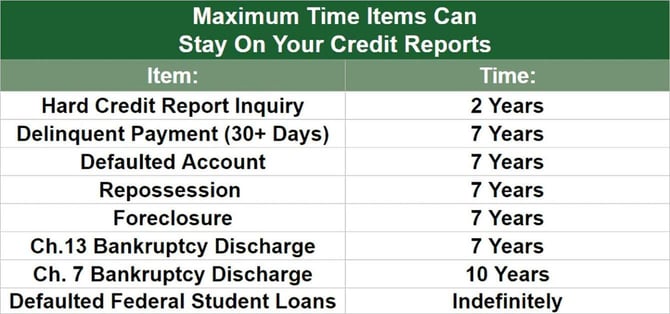

Bankruptcy is a very real, very powerful monster that haunts many adults who have experienced overwhelming debt. Once in your life, it can take up to a decade to escape a bankruptcy, which means years of dealing with bad credit, expensive loans, and quick rejections from many prime lenders, including mortgage lenders.

While you won’t need to wait for your bankruptcy to fall off your credit report completely before those mortgage lenders will let you in the door, you’ll need to take the edge off those fears by giving your bankruptcy time to “season.” This may mean waiting just a year, but it could also mean putting off a new home for four years or more.

Despite the wait, however, bankruptcy isn’t the end of your dreams of owning your own home. The effects on your credit score will dwindle with time, eventually disappearing completely, and you can work to improve your score along the way. With a little time, hard work, and responsible credit use, you can bounce back from a bankruptcy — all the way into your own home.