Writer: Eric Bank

Editor: Lillian Guevara-Castro

Reviewer: Jon McDonald

A lien is a legal claim or right against a property that secures a loan. If you are a lender, liens are an efficient way to ensure debt repayment. If you are a borrower, they are a stressful intrusion on your lifestyle that may strip you of your assets.

If you do not repay your debt, the lien holder can seize and sell your property. For example, the bank can place a lien on your house if you don’t pay your mortgage. This means the bank can take your home to recover the money you owe.

In this article, we’ll explain the different types of liens and how to resolve them.

Types of Liens

Liens can vary depending on the type of property or debt involved. Here, we will look at property liens, including mortgages, car loans, and personal property liens. Additionally, we will cover tax, judgment, and mechanic’s liens, which arise from unpaid taxes, court judgments, and unpaid labor bills, respectively.

Property Liens

Property liens are claims against real estate and similar assets. If you do not repay your debt, the individual or lender you owe can place a lien on your property. This means they have a legal right to your property until the debt is paid. There are different types of property liens based on the kind of debt.

Mortgages

A mortgage is a common type of voluntary lien. When you get a mortgage, you borrow money to buy a house. In return, you agree to give the lender a lien on the property.

The lender can seize your home if you don’t make your mortgage payments. This lien remains in place until you pay off the mortgage entirely.

This type of lien is voluntary because you agree to it when you sign the mortgage papers. It is part of the agreement to get the loan.

The lien ensures the lender can recover its money if you fail to repay the loan. This makes it easier for lenders because they know they can get their money back.

Car Loans

Another voluntary lien is when you use a loan to buy a car. The lender stakes a claim to the vehicle by placing a lien on it, meaning the car is now part of the lien process until you settle the loan.

The lender may get a judgment for the whole amount — a deficiency judgment — if the car’s repossession and sale do not net enough to cover the balance you owe.

The lien stays against the car until you repay it. You’ll need to pay the lender first if you try to sell the vehicle.

Personal Property Liens

Lenders may place liens on real estate, cars, and other valuable items such as art and jewelry. For example, if you borrow $2,000, you can use a piece of art or similar property worth that amount as collateral.

If you cannot repay the loan later, the art becomes the lender’s property.

This type of lien ensures the lender can get their money back if you don’t pay. Just as with a home mortgage or a car loan, the lender has the right to seize and sell the property you borrowed against.

Tax and Judgment Liens

Tax and judgment liens are legal claims on your property arising from unpaid debts. These liens ensure you pay taxes and court-ordered debts and can have serious financial consequences if not addressed.

Tax Liens

When you do not pay your taxes, a government authority may place a tax lien on your property. This can be for any of the three tax types — federal, state, or local. The government has a legal claim to your property and can sell your property to recover the unpaid taxes.

Tax liens damage your creditworthiness, making it difficult to establish a line of credit with lending institutions. The process can also culminate in losing your property. Unresolved tax liens can remain on your credit reports indefinitely.

Judgment Liens

A judgment lien occurs when a court determines that you must pay someone a certain amount. This includes court-mandated child support and damages awarded in a lawsuit. If, as a judgment debtor, you don’t pay your debt, the creditor can enlist the legal authorities, such as your local sheriff, to seize your property and sell it to pay the debt.

The financial consequences of judgment liens can be profound. They can significantly impact your credit score and make it difficult to do much with your property. An excellent way to avoid serious trouble with a judgment lien is by paying off the underlying debt as soon as possible.

Recent Changes

On July 1, 2017, credit bureaus made a significant change to improve the accuracy of credit reports. This change was part of the National Consumer Assistance Plan (NCAP). It resulted from agreements with state attorneys general and the Consumer Financial Protection Bureau (CFPB).

It states that public records such as tax liens and civil judgments must include detailed personal information, such as your Social Security number or date of birth, to appear on your credit report. Many older records lack this information, so the credit bureaus have removed many liens from consumer credit reports.

In fact, Experian, Equifax, and TransUnion removed about 50% of tax liens and most civil judgments from credit reports. This change reduces errors and makes reports more accurate.

Financial Impact of Liens

Liens can be seriously distressing and problematic because they may lead to personal property or home loss. Individuals facing this situation should seek support not only to help protect them financially but also to plan a way out of what could become an ongoing issue.

Credit Score Damage

Negative entries on your credit report include liens. They appear in the public records section, showing that you have an outstanding debt covered by law. Having this in your credit report signals lenders that you are a credit risk.

Your credit score can severely drop when you carry a lien. You may lose around 100 points, although this isn’t set in stone; the effect can actually be even worse.

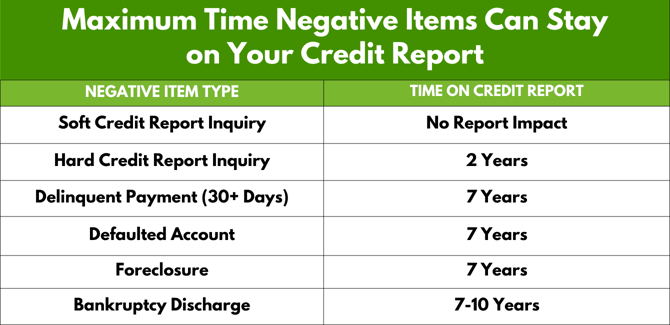

Liens can remain on a credit report for a long time, up to seven years from the filing date. Tax liens that you have not paid can linger on your reports indefinitely. They can make it challenging to borrow money or get approved for good credit cards.

Property Sale Restrictions

Buying and selling property is a complicated process, made even more difficult by the existence of liens. Before a sale can proceed, the seller must clear up any and all liens on the property.

Disclosure Requirements

Disclosure laws are a list of requirements of what must be known about a property put up for sale. Property owners have a legal duty to disclose certain things about a property to its buyer.

Unlike the law on advertising, which is generally riddled with exceptions, the duty to disclose is far more concrete. It requires that you, at minimum, let a buyer know of certain simmering controversies around the property or claims against it.

Impact on Sale

The sales process can become complicated when a lien is involved. This is because the sale can’t close until the lien is resolved. Since it’s attached to the property, the lien will remain in place regardless of who the buyer is.

A property with a lien conveys a financial risk to the prospective buyer. This should give buyers pause, which may mean that a property takes longer to sell and potentially sells for less.

Liens add a layer of complexity that the prospective buyer must carefully consider.

Payoff at Closing

A lien can delay the closing and complicate the resolution. The seller often knows the amount of the lien at this stage, but the buyer might not.

Not only must the lien be paid off, but you must also prove that you have paid it in full.

The closing agent or attorney ensures the lien is fully paid before the property can be transferred to the buyer. It is of utmost importance to guarantee lien-free ownership to the purchaser.

Effect of a Mechanic’s Lien

A contractor or builder can place a mechanic’s lien on a property when they don’t receive full payment for their work. This type of lien can prevent the sale of the property until the debt is paid.

It can also affect the property’s value and marketability. Suppose you are buying a property with a mechanic’s lien.

In that case, you must resolve it before purchase to avoid taking on the previous owner’s debt.

Poor Personal Loan Rates & Terms

Personal loans may be secured by property, securities, or cash. As with mortgages and auto loans, the lender can place a lien on the loan’s collateral.

Collateral Requirement

Lenders require collateral for secured loans. Collateral is an asset, such as a car, house, securities, or cash, that you offer the lender to secure the loan. The lender can seize the collateral to recover the money if you fail to repay the loan,

Collateral reduces the risk for the lender and often allows consumers to get better loan terms, such as lower interest rates. Offering collateral can also help you get approved for a loan if you have a lower credit score.

Interest Rates

Liens can impact the interest rates on your loans. Lenders see you as a higher risk if you have a lien on your property. This is because a lien indicates you have unpaid debts.

As a result, lenders may charge higher interest rates to offset this risk. Higher interest rates mean you will pay more over the life of the loan. Clearing liens before applying for new loans can help you obtain better interest rates.

Risk of Default

The lender can take legal action to recover their money if you default on a loan. For secured loans, the lender can seize the collateral you offered.

For example, if you use a car title as collateral and default on the loan, the lender can repossess your vehicle. For unsecured loans, the lender can place a lien on your property or take other legal actions to collect the debt.

Defaulting on a loan can also damage your credit score, making it harder to get loans in the future.

How to Resolve Liens

You can resolve a lien by repaying it or disputing it. Paying off the debt is straightforward, whereas disputing liens can be tricky unless you have documentation to back up your story.

Pay Off the Debt

Paying off debt is the most direct way to resolve a lien. The following list outlines the main methods to pay off liens. These include negotiating a settlement and obtaining a lien release:

- Pay Off the Debt: Confirm with the lienholder the total amount of money you owe. Ensure that you pay through the proper channels and follow any specific instructions. Keep a detailed record of all the communications and payments, as you may need it later. Request a written confirmation from the lienholder that your payment is complete.

- Settlement Options: Talk directly with the lienholder about the possibility of settling your debt for less than the total amount. Clearly explain your financial situation to the lienholder and offer them a sum based on what you can afford to pay. Work to reach an agreement with the other party detailing the reduced amount and payment terms.

- Release of Lien: After the lien is paid off or settled, request a lien release document from the lienholder. Ensure the lien release document is notarized if required. File the lien release document with the appropriate local government office, such as the county recorder or land registry. Keep a copy of the filed lien release document for your records to prove the lien has been resolved.

Paying off a lien can be expensive, but failing to do so can be highly damaging and, ultimately, cost more money.

How to Dispute a Lien

Disputing a lien involves identifying errors, seeking legal help, and following a formal resolution process. The list below outlines these steps to help you effectively contest and resolve a lien on your property:

- Identify Errors in Filing: Ensure the lien document is free from ordinary errors, such as amounts that need to be correctly entered, wrong dates, or names that need to be spelled correctly. Collect evidence that allows you to prove that the errors exist and are not simply your attempt to gain an advantage. If what you are trying to prove doesn’t look ironclad, don’t include it.

- Legal Assistance: Suppose the lien is incredibly complicated, or the lienholder is stubborn and won’t fix any mistakes. In that case, you should consider seeking legal help. An attorney can help you better understand your rights. Ideally, you may need to find a real estate attorney or a property lawyer with experience with lien litigation.

- Resolution Process: First, you should make your disapproval of the lien known to the lienholder. Furnish them with all the proof you have that they’ve made a mistake. Make your case to the governing office at the local level responsible for recording the lien. Follow up to ensure the process reaches a conclusion.

If you contest a lien, you should have a valid reason. Otherwise, you’re just wasting time and money.

Liens Have an Important Purpose

Liens are financial tools that lenders or the government can use to protect their interests. Though they can be frustrating for the debtor, they allow access to better loan terms and interest rates and allow them to use their property while the loan is being repaid.

They also add an extra layer of protection against financial fraud, allowing people owed money due to legal settlements or unpaid work to get at least a portion of the money they are entitled to.

To protect your property and your credit score, it is essential to stay on top of any debts. Otherwise, your creditor may sell your property, leaving you high and dry.

Up When it Comes to Your Debt")

& What It Means")