Writer: John Ulzheimer

Editor: Jon McDonald

Reviewer: Ashley Fricker

This is an excerpt from a recent Q&A with renowned credit expert John Ulzheimer. You can see the entire interview on our YouTube Channel.

“There are two types of bankruptcies that will generally appear on a consumer credit report. They are, obviously, the two consumer bankruptcies, Chapter 13 or Chapter 7 bankruptcy.

Chapter 13 is also referred to as a wage earner plan. This means you make enough money, I don’t want to say too much money because I don’t know that there’s really such a thing, that you have to pay the trustee, the bankruptcy trustee, which then distributes your payments to your creditors. So even though they’re not getting back everything that you owe them, they are getting back some of what you owe.

Chapter 13 bankruptcy, the actual record of the filing, will remain on a credit report for no longer than seven years.

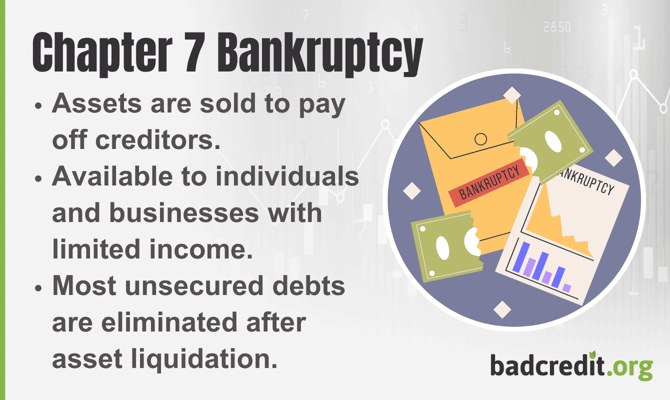

A Chapter 7 bankruptcy, which some people call either a straight bankruptcy or essentially a complete liquidation of your statutorily dischargable debts, usually means things like credit card debt, medical debt, collections, things like that.

Generally speaking, government debt is not dischargeable; things like federal tax liens and federally guaranteed student loans have a much harder time discharging those than the non-governmental debts.

And Chapter 7s are for consumers who, generally speaking, make a lower income and so they can’t afford to pay back their creditors much, if at all. And therefore, the court approves this complete liquidation of their dischargeable debts. A Chapter 7 bankruptcy will stay on your credit report for up to 10 years, so a decade.

Now, in addition to the actual public record, which is its own complete separate thing on your credit report, you have all of the debts that are discharged or included in your bankruptcy. Those can’t stay for 10 years, even if you have a Chapter 7 bankruptcy.

The rules with respect to how long debts that are in what’s called a terminally delinquent status — so collections, defaults, repossessions, charge-offs, things like that. The rules are the same regardless of whether you have filed bankruptcy or not. And the rules for those are seven years. Seven years from the date that you went delinquent and never cured the account.

So when you compare the bankruptcy filing — the public record versus the debts that were included in the bankruptcy — it’s very, very likely that the debts that are included in the bankruptcy are going to be off your credit report before the record of the filing, especially and almost guaranteed with a Chapter 7.

Remember, Chapter 7 can stay on a credit report for three years longer than negative information, which can only stay up to 7 years. Chapter 7 can stay up to 10 years. So that’s the bad news. Okay, so now let’s start talking about the good news.

There’s a reason why we have a bankruptcy code in the United States, right? If you’ve looked at any of the surveys that have been done over the years that try to find out why consumers file bankruptcy, there’s a lot of reasons why. And it’s not always, hey, he’s a deadbeat. That’s actually kind of like on the lower end of the list.

Things like, you know, sickness in the family, extended unemployment, a failed business venture, divorce. So there are a lot of reasons why consumers can feel the need to take advantage of the bankruptcy statutes.

And it’s not always because that they’re just really bad with managing their credit cards. Certainly there are certain examples like that, but you shouldn’t always equate bankruptcy with deadbeat.

Because of that, the answer regarding how quickly can my credit scores recover is actually probably more surprising than you may think. It is not uncommon for consumers’ credit scores to start to recover 24, 36 months after the bankruptcy filing.

And here’s why — specially in a Chapter 7 scenario, which is that straight bankruptcy scenario: Guess how much debt you have once your Chapter & bankruptcy has been discharged?

You don’t have any unless you have tax liens, which aren’t on your credit report, by the way, because tax liens have been off credit reports for a very long time. Unless you have federally guaranteed student loans, and those will certainly still be on the credit report.”

To put that in perspective, here are how long some other items can stick around on your credit reports compared to bankruptcies:

| Item Type | Time on Credit Reports |

|---|---|

| Soft Credit Report Inquiry | No Report Impact |

| Hard Credit Report Inquiry | 2 Years |

| Delinquent Payment (30+ Days) | 7 Years |

| Vehicle Repossession | 7 Years |

| Defaulted Account | 7 Years |

| Foreclosure | 7 Years |

| Chapter 13 Bankruptcy | Up to 7 Years |

| Chapter 7 Bankruptcy | Up to 10 Years |

“But if you don’t have student loans and you just had things like, personal loans or medical collections or defaulted credit cards, all the balances associated with those are now zero. So you immediately get the benefit of having zero balances across all these negative accounts that previously, before you actually filed your bankruptcy, had some balance greater than zero.

Because that’s the whole purpose of the bankruptcy is it protects you from your creditors trying to collect those debts.

TransUnion has even published some studies about this over the years that consumers’ credit scores start to become fairly respectable [over that 24 to 36 month period]. And when I say respectable, we’re not talking FICO 800. That’s going to take a lot of time. But it’s not unusual [to see] FICO in the low 600s, FICO in the mid-600s.

And that means that you’re bankable and you can get a car loan. It means you’re bankable and you can get a mortgage. It means you’re bankable and you can get a credit card.

“It is not uncommon for consumers’ credit scores to start to recover 24, 36 months after the bankruptcy filing.”

You may not be getting kind of like what I call the “apex predators” of loans and credit cards and interest rates, but if you think that you’re stuck with payday loans and asset borrowing, that is wrong.

You’d be surprised how quickly you’re going to start getting respectable offers from mainstream, well-known lenders [that] have programs for consumers who have what I call kind of bruised credit.

And as long as you manage those properly and don’t get back into the type of debt that maybe you were in prior to your bankruptcy, you’d be surprised how quickly you can recover. Certainly, you’re not gonna have to wait 10 years for the bankruptcy to fall off; you’ll be bankable way before then.”