Adam has written, edited, and managed content for news outlets and digital publications for nearly 20 years. Since specializing in finance in late 2016, his editorial focus has been on consumer financial literacy. Adam is most knowledgeable in the areas of credit scores, financial products and services, and the banking industry.

Lillian brings more than 30 years of editing and journalism experience, having written and edited for major news organizations, including The Atlanta Journal-Constitution and the New York Times. A former business writer and business desk editor, Lillian ensures all BadCredit.org content equips readers with financial literacy.

Ashley has managed content strategy for BadCredit since 2015, partnering with major banks, financial institutions, and media outlets to deliver authoritative personal finance content. Her expert credit card commentary has appeared in top national publications, including CNBC, MarketWatch, Investopedia, Yahoo Finance, and Reader's Digest, establishing her as a trusted voice in the industry.

Auto loans for bad credit can help borrowers with poor credit scores finance a new or used vehicle. The lenders and loan networks featured here offer fast online applications, flexible requirements, and financing options for consumers who are rebuilding credit. Here are our experts’ picks for the best auto loans for bad credit.

Disclosure: When you apply through links on our site, we often earn referral fees from partners. For more info, see our ad disclosure and review policy.

BadCredit.org’s auto loan ratings are based on our experts’ evaluation of factors including interest rates, loan fees, and approval odds. We also consider the loan terms and vehicle restrictions. Our ratings are unbiased and regularly updated.

BadCredit.org’s auto loan ratings are based on our experts’ evaluation of factors including interest rates, loan fees, and approval odds. We also consider the loan terms and vehicle restrictions. Our ratings are unbiased and regularly updated.

BadCredit.org’s auto loan ratings are based on our experts’ evaluation of factors including interest rates, loan fees, and approval odds. We also consider the loan terms and vehicle restrictions. Our ratings are unbiased and regularly updated.

BadCredit.org’s auto loan ratings are based on our experts’ evaluation of factors including interest rates, loan fees, and approval odds. We also consider the loan terms and vehicle restrictions. Our ratings are unbiased and regularly updated.

BadCredit.org’s auto loan ratings are based on our experts’ evaluation of factors including interest rates, loan fees, and approval odds. We also consider the loan terms and vehicle restrictions. Our ratings are unbiased and regularly updated.

BadCredit.org is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free for users, we receive advertising compensation from the financial products listed on this page. Along with key review factors, this compensation may impact how and where products appear on the page (including, for example, the order in which they appear). BadCredit.org does not include listings for all financial products.

Our Editorial Review Policy

Our site is committed to publishing independent, accurate content guided by strict editorial guidelines. Before articles and reviews are published on our site, they undergo a thorough review process performed by a team of independent editors and subject-matter experts to ensure the content’s accuracy, timeliness, and impartiality. Our editorial team is separate and independent of our site’s advertisers, and the opinions they express on our site are their own. To read more about our team members and their editorial backgrounds, please visit our site’s About page.

Review Breakdown: Bad Credit Auto Loans

Need a car or truck loan but lack the credit history most lenders prefer? Below is a summary of the top auto loan providers for people with a poor credit score. To apply for auto financing online, simply click on the name of the service provider to visit its easy online application. These loan services provide quick approval and specialize in helping those with poor credit.

BadCredit.org’s auto loan ratings are based on our experts’ evaluation of factors including interest rates, loan fees, and approval odds. We also consider the loan terms and vehicle restrictions. Our ratings are unbiased and regularly updated.

BadCredit.org’s auto loan ratings are based on our experts’ evaluation of factors including interest rates, loan fees, and approval odds. We also consider the loan terms and vehicle restrictions. Our ratings are unbiased and regularly updated.

BadCredit.org’s auto loan ratings are based on our experts’ evaluation of factors including interest rates, loan fees, and approval odds. We also consider the loan terms and vehicle restrictions. Our ratings are unbiased and regularly updated.

BadCredit.org’s auto loan ratings are based on our experts’ evaluation of factors including interest rates, loan fees, and approval odds. We also consider the loan terms and vehicle restrictions. Our ratings are unbiased and regularly updated.

BadCredit.org’s auto loan ratings are based on our experts’ evaluation of factors including interest rates, loan fees, and approval odds. We also consider the loan terms and vehicle restrictions. Our ratings are unbiased and regularly updated.

Auto loans for bad credit can help borrowers with poor credit scores finance a new or used vehicle. Here’s what to know about qualifying, comparing lenders, and managing the cost of financing with bad credit.

Reduce the hassle with a little expert insight into how borrowers with bad credit can still qualify for auto financing.

1. Can I Get an Auto Loan With Bad Credit?

Yes. Many lenders are willing to extend auto loan offers to borrowers who have bad credit scores.

This is partly because, unlike most personal loans, an auto loan is secured. This means that the vehicle you purchase is also used as collateral to secure your loan. If you stop making payments or default on the loan altogether, the lender can repossess the vehicle and sell it to recoup some of its losses.

Because lenders can offset some risk, they may be more willing to consider applications from borrowers with credit issues.

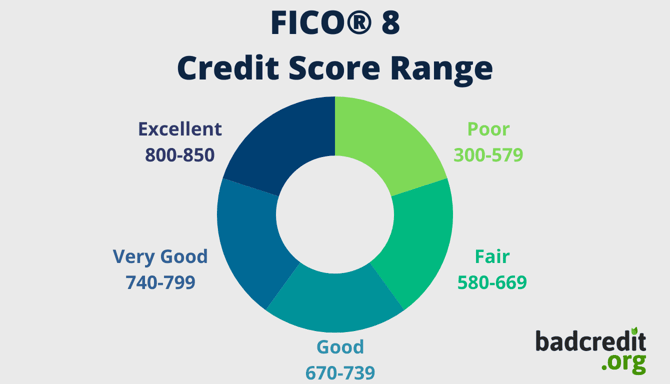

It’s important to remember that not all bad credit is the same. Your FICO credit score can range from 300 to 850. A score under 580 is generally seen as poor credit (that’s what FICO refers to as bad credit). Let’s take a closer look at FICO’s credit score tiers:

Lenders who specialize in auto loans for bad credit borrowers, often called subprime auto lenders, may consider your application if you have a credit score in the 500s. At 500 or below, your options may dwindle.

2. Can I Get Approved for a Car Loan With a 500 Credit Score?

If your credit score is 500 or lower, finding a lender willing to work with you can be challenging. And even if you get approved for financing, expect the interest rates to be quite high. The good news is, you can improve your chances and potentially get better rates and terms by:

Adding a trade-in vehicle: The inclusion of a trade-in can lower the loan amount and increase your stake in the purchase. That means you’ll have to borrow less and have more invested in the loan.

Making a down payment: Auto lenders don’t like to be the only ones taking on risk. When you include a down payment, you show that you have skin in the game and are serious about handling your debt.

Enlisting the help of a cosigner: A cosigner is someone who is willing to sign for your loan to guarantee that you will repay the debt, typically someone with much better credit. Just be sure to stay on top of your loan payments because a late payment or default will hurt your and the cosigner’s credit scores, which could also fracture friendships and family ties.

You may also find yourself struggling to find a loan if you have no credit history, which means you haven’t had enough information reported to the credit bureaus to generate a credit rating or score. You may not have financial mistakes on your credit reports, but you don’t have a past that a lender can view.

3. Which Banks Offer Auto Loans For Bad Credit?

Many traditional banks have stricter underwriting standards for borrowers with bad credit.

A credit union, on the other hand, is a member-owned institution that returns all of its profits back to its members. While this means more affordable financial products and more lenient loan approvals, it doesn’t mean someone who has bad credit is guaranteed a loan.

Here are some of the primary differences between banks and credit unions:

Banks

Credit Unions

For-profit institutions owned by shareholders

Not-for-profit institutions owned by members

Anyone can open an account

Only members can open an account

Typically higher fees and interest rates

Typically lower fees and interest rates

May be located nationwide, with branches in most cities

Often local with branches in certain communities or regions

Deposit insurance provided by the FDIC (Up to $250,000)

Deposit insurance provided by the NCUA (Up to $250,000)

Expect a modern website and responsive mobile app

Technology may be available but not as advanced

Most credit unions limit their loans to members who have fair credit or better. That means a FICO score of 580 or higher. But that doesn’t mean you’re out of luck — many independent lenders consider financing applicants who have bad credit.

4. What Interest Rate Will I Pay for a Bad Credit Auto Loan?

Bad credit borrowers will pay the highest interest rates for auto loans, but the actual rate depends on market conditions and other economic factors.

Your credit score plays a significant role when auto lenders set out to determine your interest rate because it clearly highlights your risk as a borrower. Finance options for poor-credit consumers can climb to higher than 21% for used car loans.

That’s nearly four times greater than the lowest average interest rates offered to borrowers purchasing new cars with excellent (or superprime) credit. Here is a look at the average auto loan interest rates by credit score:

Category

Credit Score Range

New Car

Used Car

Superprime

781 – 850

4.88%

7.43%

Prime

661 – 780

6.51%

9.65%

Near prime

601 – 660

9.77%

14.11%

Subprime

501 – 600

13.34%

19.00%

Deep subprime

300 – 500

15.85%

21.60%

Source:Experian, data as of Q3 2025; scores calculated using VantageScore 4.0.

Shopping around with lenders that offer prequalification can help you compare estimated rates without submitting multiple full applications right away.

Over the course of an auto loan, these interest rates can mean paying thousands of extra dollars because you have bad credit. How much you ultimately pay also depends on your loan term, or the length of the loan.

Because bad credit borrowers pay such high interest rates, many choose longer loan terms to keep their monthly payments affordable. But this also costs much more money in the long run — as we will discuss later.

5. Can I Buy a New Car With Bad Credit?

You may still qualify for a loan to purchase a new car if you have bad credit, but it could hinge on other factors, including down payment, trade-in value, your income, and whether you have a cosigner.

If you have a very low credit score, such as below 500, you will have trouble finding a loan without a large down payment or a cosigner. A score above 550 could give you a better chance of qualifying for a new car loan, but new car loans for bad credit borrowers have plenty of hurdles.

In either scenario, you will still likely need to include a substantial down payment or a trade-in to lower your overall loan amount. Few lenders, if any, will lend 100% of a new vehicle’s price to someone who has bad credit.

Even with bad credit, you may still have options for financing a vehicle. Comparing lenders, making a down payment, and borrowing only what you can afford can help you secure a loan that fits your budget and supports your long-term financial health.

About The Author

Adam WestContributing Editor

Adam West is a finance editor for BadCredit.org, where he has interviewed over 500 financial experts and industry movers and shakers to report the latest information, news, and advice on topics related to helping subprime borrowers achieve greater financial literacy and improved credit scores. Adam has more than a dozen years of editing, writing, and graphic design experience for award-winning print and online publications, and specializes in the areas of credit scores, subprime financial products and services, and financial education.

Information Warranty & Disclosure: Great efforts are made to maintain reliable data on all offers presented. However, users should check each provider’s official website for updated terms, details and conditions for each offer before applying or signing up. Our site maintains strict terms of service and may accept compensation for paid ads or sponsored placements in accordance with these terms. Users must be at least 18 years of age to be eligible for financial offers as per the terms presented on provider websites.

* FICO scores/credit scores are used to represent the creditworthiness of a person and may be one indicator to the credit type you are eligible for. However, credit score alone does not guarantee or imply approval for any financial product.