Writer: Jon McDonald

Editor: Austin Lang

Reviewer: Ashley Fricker

Nobody’s perfect, least of all when it comes to personal finances. You may struggle to stick to your budget, handle your debts, or remember to pay off expenses before they’re due. And if you forget to pay your bills before they’re due, you’ll have to make a late payment.

When you pay your bill after the due date but before the end of your next billing cycle, it’s considered a late payment. A late payment is a bill payment made after your statement’s due date.

Late payments are bill payments that are made after your due date. Depending on how late they are, they can incur extra fees and even hurt your credit.

As a rule of thumb, you want to avoid late payments and always pay at least the minimum due on your cards. But life happens, and making a late payment doesn’t mean complete financial ruin. The consequences of late payments — both with lenders and the credit bureaus — depend on how far past the due date you make the payment.

If you’ve had to make a late payment, don’t panic; you can still fix it. I’ll help you understand your options so you don’t let a temporary problem become a massive financial headache.

What to Expect When You Make Late Payments

When you’re late for a bill payment, you should expect some financial consequences. These are relatively minor, especially when you pay your bill before it’s considered “missed.” But typically, you have three potential penalties to watch out for: late payment fees, interest rate increases, and hits to your credit.

Late Payment Fees

Unfortunately, forgetting your bills might make you familiar with everyone’s least favorite charge: late fees. No matter how far past due your bill is, you’re likely to encounter late fees.

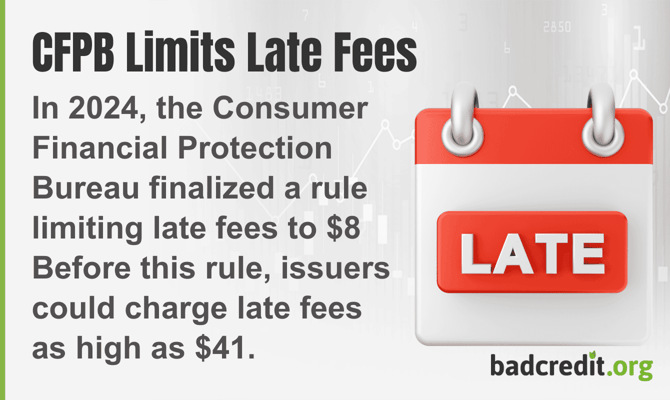

But there’s good news. The Consumer Financial Protection Bureau (CFPB) closed a loophole and made it harder for banks to charge excessive late fees. The new ban reduced a standard late fee from $32 to $8.

Late fees are supposed to only account for the creditor’s increased costs in collecting late payments, and the $8 charge is likely closer to the actual cost for banks.

Still, that $8 can be annoying, especially when money’s tight to begin with. I recommend asking your creditor to drop the late fee. It doesn’t always work, but then again, it might!

Interest Rate Penalties

If you carry a balance on your credit card, you may face a consequence of late payments worse than a late fee: a penalty APR (annual percentage rate). A penalty APR raises your interest rate, generally, to around 29.99%. Yikes.

The CARD Act requires card issuers to give you a 45-day notice before your penalty APR kicks in. If you had an introductory APR or other promotion, you can kiss that goodbye.

The CARD Act requires credit card issuers to give you a 45-day notice before they start charging a penalty APR. You could receive this notice shortly after missing a payment.

That said, your creditors have to review your account every six months following a penalty APR rate increase. If you’ve made your payments on time, they could reinstate your original APR (but not the promotional APR).

Negative Credit Score Impact

Late payments may affect your credit score.

Before your late payment goes onto your credit report — generally in the 30 days following your due date — you may still have time to make the payment before your creditor reports it to the credit bureaus. Some creditors will still report the late payment, but others won’t.

The severity of the hit to your credit depends on how late you make the payment. Generally speaking, there’s a significant difference between payments made 30, 60, 90, 120, 150, or 180 days past due.

Here is a chart that explains the timeline of missed payments and when issuers take certain actions:

| 30-59 Days Late | 60-179 Days Late | 180+ Days Late |

|---|---|---|

| Bank will charge another late fee | Bank continues to charge late fees | Account closed |

| Penalty APR likely goes into effect | Your account may be closed | Debt sold to collections agency or other debt buyer |

| Account reported to the major credit bureaus as late | Accounts later than 90 days considered seriously delinquent | Bank may sue you |

| Your credit score will start to drop | Account may go to collections | Defaulted account remains on your credit report for seven years |

After 180 days (or six months), your creditor may label the missed payment a “charge-off,” in which they assume the bill won’t be paid due to severe delinquency. This creates a major hit to your credit score and may result in them sending a debt collector after you. I can speak from personal experience: This is not fun.

When a Payment Considered Late

Even if you only miss your due date by one day, it’s still considered late. While this may result in a late fee, it is unlikely to have a severe impact on your credit score. If you’re a few days late on your credit card payment, make sure to get that in as soon as possible.

Your Billing Cycle and Due Date

Most credit cards or repeat bills have a month-long cycle. At the end of each billing cycle for your credit cards or other repeat bills, you’ll get an account statement with a due date. Once you get your statement, you usually have 30 days to make a payment before it’s considered late.

When you miss your due date, your payment is officially late. But credit card issuers don’t report it to the credit bureaus until it is 30 days late — so you still have time.

If you don’t pay the minimum payment by your due date, you’re officially late on your payment. But creditors won’t report your late payment to the credit bureaus until the reporting date, usually 30 days after your due date.

Paying More Than 30 Days Late

Your next billing cycle will end 30 days after your payment due date. This signals that your payment has moved from “late” to “missed.” At this point, your creditor will notify the credit bureaus.

The missed payment will probably drop your credit score. But if you already have poor credit, this probably won’t make a huge difference yet.

60 Days Late and Beyond

After 60 days, the hit to your credit will become more severe. Your APR will likely go up if it hasn’t already — and the negative mark will remain on your history for a while. Here is a look at how long late payments and other negative items can stay on your credit reports:

| Negative Item Type | Time on Credit Report | |

|---|---|---|

| Soft Credit Report Inquiry | No Report Impact | |

| Hard Credit Report Inquiry | 2 Years | |

| Delinquent Payment (30+ Days) | 7 Years | |

| Defaulted Account | 7 Years | |

| Foreclosure | 7 Years | |

| Bankruptcy Discharge | 7-10 Years | |

The biggest consequences come when your creditor charges off your debt, usually after 180 days. A charge-off is a huge blow to your credit. You may have to deal with debt collectors contacting you and, under the worst circumstances, taking legal action against you.

How to Prevent Late Payments

One late payment doesn’t need to be a huge deal, but habitual late payments probably will be. After your first (or most recent) late payment, I suggest taking a moment to assess your finances and set up checks to make sure this doesn’t keep happening.

Set Up Automatic Payments

Automate, automate, automate: Financial experts love to talk about automating every part of your finances, from saving for retirement to paying your bills. You may tune them out, but they’re right. The easiest way to fix your finances is to automate everything.

Set up an automatic payment to make sure that at least your credit card minimum monthly payment gets paid without you ever thinking about it.

I prefer not to pay my entire credit card balance automatically. I only keep enough for my basic expenses in my checking account at any given time (Hello, high-yield savings accounts!). But if you keep enough money in your checking account to always cover your credit card statements, you can set your accounts to be automatically paid in full each month.

Just remember to glance at your statements so you can notice any irregular charges.

Use Budget and Payment Reminders

Automating your payments only helps if you have a sufficient payment source to pull from. Late payments are often a product of simple forgetfulness, but they can also be the result of living beyond your means and not having the funds to pay your debts.

If your credit card balance is higher than you can afford, work out a new budget that actually makes sense for your wallet. Do what you can to avoid taking on new credit card debt.

Keep an eye on when you get paid. Set up payment reminders to pay your bills right away so that you never miss a payment or overestimate how much cash you have to spend.

Contact Creditors If You May Be Late

If you know you’re not going to be able to make the minimum payment before your due date, try not to freak out. You don’t have to be a sitting duck; you can alert your creditor that you’re going to be late on payments this month.

Helpful tip: Call your creditor’s customer service line and see if they can work with you to find a solution. They may change the due date for you, waive the late fee, or lower the minimum payment you need to make.

Dealing With a Late Payment

When you realize your payment is late, don’t bury your head under the sand. This is a problem that definitely gets worse the longer you ignore it, so make sure to take action ASAP.

Pay as Soon as Possible

The most important part of dealing with a late payment is paying immediately. The longer you wait, the worse the consequences will be.

Remember that if you make your payment within the first 30 days past your due date, your mistake likely won’t hit your credit score or raise your APR. Sure, you won’t exactly be popular with your credit card company, but who is?

Request a Fee Waiver

If you miss your due date, you’ll probably find a late fee on your bill. Depending on your financial circumstances, this could be a minor annoyance or a tough blow.

Consider calling your creditor and requesting a fee waiver. Talking to customer service can be a pain, but it’s worth the savings.

Many creditors will waive your late fee if you request it, especially for a first-time late payment.

Make sure to have the reasons you deserve a fee waiver ready to go. If this is your first late payment, highlight that. Let them know any extenuating circumstances that prevented you from making your payment this month or any anomalies that make it less likely you’ll repeat this in the future.

In my experience, people are usually willing to help when you advocate for yourself. Most people stay quiet. It may be cliche, but the squeaky wheel really does get the grease.

Keep an Eye on Your Credit Report

No one likes to think about their credit, but you definitely should pay attention to it. Regularly checking on your credit will help you notice any changes to your credit, whether from a missed payment, high rotating utilization, or the worst possibility: fraud.

You can check your credit for free as often as weekly at AnnualCreditReport.com, and you can also pay for services that monitor your credit more vigorously. Many credit card companies will let you see an estimate of your credit score for free each month.

You may have heard that checking your credit lowers it, but that isn’t true. Only hard credit checks — applications from potential creditors to give you credit — lower your credit. Checking your own credit is a soft check and won’t hurt your credit.

Set Up a Plan to Avoid Costly Late Payments

Late payments add up. From late fees to higher APRs to lower credit, the penalties that come from racking up late payments can quickly put a damper on your financial future.

Set up safeguards to make sure you never miss a due date again. Automate your minimum monthly payments, and set reminders to pay the rest of your credit card balance. If you have credit card debt, come up with a plan to pay it off over time and stop adding to it.

You can’t control everything about your finances. The scary reality is that you never know when you’ll total your car, end up in the hospital, or lose your job. Most of us are a few moments of bad luck away from some real financial havoc.

But making your payments is one thing that you can control. Once you create a payment system that works for you, late payments are just one less thing you need to worry about.