Writer: Mike Senecal

Editor: Lillian Guevara-Castro

Reviewer: Adam West

Key Takeaways

- A new study by FICO and BNPL provider Affirm shows that the use of BNPL products can improve credit scores for some borrowers.

- FICO's plan to include BNPL transactions in credit score products promises to drive score increases while improving model risk performance.

- The results of the FICO/Affirm study depend on the relatively high percentage of subjects with near-prime or higher credit scores compared to the market as a whole.

This past January, I reported the results of a Consumer Financial Protection Bureau (CFPB) study associating frequent users of Buy Now, Pay Later (BNPL) services with overuse of credit cards and other forms of credit.

Since then, FICO has teamed up with leading BNPL provider Affirm to produce research that calls many of the CFPB’s conclusions into question. The 12-month study simulated the inclusion of Affirm BNPL loans into consumers’ credit reports and found little or no impact on scores.

On the basis of those results, FICO also announced it was developing a methodology to include BNPL transactions in credit scores. It makes sense: The industry needs more accurate consumer risk assessment to differentiate borrowers and allow providers to extend credit more confidently.

The Biden-era CFPB’s view of the BNPL industry does not accurately reflect Affirm’s customer base of 71% near prime and above.

Of course, we can’t forget another event that took place between the arrival of the CFPB report in January and the FICO/Affirm report in February: the ascension of President Donald Trump and the Republican congressional majority.

Now, the version of the CFPB that called BNPL use into question is no more. Naturally, I wanted to understand whether the differences in the CFPB and FICO studies extended beyond the CFPB’s typical overreach during the Biden administration.

Surprisingly, I found the studies were about two different worlds. At the time of the FICO/Affirm announcement, Affirm published a fascinating blog entry to help us understand how BNPL is maturing.

The CFPB report “aggregates information from six fundamentally different companies to make broad generalizations about an industry and population,” wrote Affirm’s Chief Legal Officer Katherine Adkins in the blog. “While the CFPB report suggests that borrowers with subprime or deep subprime credit scores make up the majority of BNPL originations across the industry, it’s important to note that this isn’t representative of all providers.”

CFPB, BNPL, and Credit Overuse

BNPL gained traction by appealing to subprime and thin-file consumers who lacked access to traditional credit. But providers like Affirm now increasingly target near-prime and even prime consumers (representing borrowers with FICO scores above 620).

It’s all in the data and in the way Affirm explained it in the blog. The differences between what the CFPB concluded and what FICO and Affirm observed tell us what we really need to know: The face of BNPL is changing.

Getting the data was no easy feat for the CFPB, I said when we first looked at its study results. Although some BNPL providers may report certain types of financing arrangements to the bureaus, particularly those that involve interest or extended repayment periods, they generally don’t report the short-term, interest-free installment loans consumers (particularly younger consumers) are gobbling up in increasing numbers.

This lack of reporting can be a double-edged sword. It helps consumers avoid potential negative credit impacts from missed payments, but it also means that on-time payments generally don’t contribute to building credit. The CFPB used its oversight powers to compel six BNPL providers to provide de-identified data for its study.

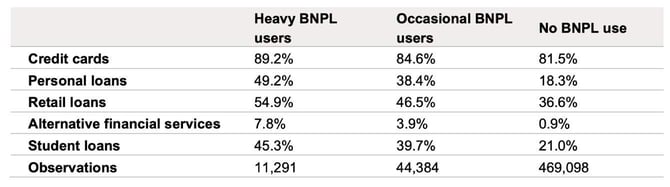

That snapshot of data revealed that 65% of BNPL customers from 2021 to 2022 had subprime or deep subprime credit scores (or not enough credit history to generate a score). Providers approved 78% of BNPL applications from customers in those categories.

BNPL borrowers held higher amounts of other forms of debt, including personal loans, retail loans, student loans, credit cards, and so-called “alternative financial services” loans. And subjects had higher credit card utilization rates before adopting BNPL, suggesting they were need-driven.

Almost lost in the shuffle, it seems, was the fact that the data came from 2022, practically ancient history when it comes to the BNPL industry. Affirm and five other providers responded to the CFPB’s market monitoring orders in March 2023.

But only in January 2025 did the CFPB publish its results, characterizing BNPL as a less desirable alternative solution.

“Consumers may be relying on BNPL when other credit is unavailable,” the study stated.

An Industry Shifting to Near Prime and Above

The question is whether that’s still true — if it ever was. FICO and Affirm based their study on data from Affirm’s fiscal year 2024. For me, it’s clear the CFPB’s perspective is a reminder of the past rather than a harbinger of the future.

FICO and Affirm couldn’t look at the type of anonymized consumer credit data the CFPB could compel companies to provide. So they did the next best thing, simulating what would happen to the credit scores of more than 500,000 customers who had taken out at least one Affirm BNPL loan during the study period.

The study compared those simulated scores against a benchmark population of non-Affirm customers and found that:

- Impacts on scores were “generally consistent with the opening of a new account,” meaning less than 10 points higher or lower for more than 85% of study subjects.

- Contrary to the CFPB, a majority of frequent customers (defined as those who had recently obtained five or more Affirm BNPL loans) had higher scores or no score changes.

- Impacts on FICO score predictiveness ranged from modest improvement to no adverse effects across different use cases.

Why? In contrast to the CFPB sample, where only 35% of study subjects had scores of near-prime or above, 71% of Affirm customers were at that status, Adkins wrote in the Affirm blog article.

And while the CFPB found that BNPL customers tended to default much more frequently on their credit card loans (10%) as opposed to their BNPL loans (2%), Adkins declared Affirm’s “dramatically lower” default rates for Affirm products were “driven by several major advantages — that are both structural and the result of significant investment.”

The transaction-level underwriting approach at Affirm, Adkins wrote, allowed it to responsibly extend credit to more consumers by requiring down payments and offering lower credit amounts.

The FICO/Affirm study found score impacts from BNPL use were generally consistent with the impact from new account openings (+/- 10 points for 85% of study subjects).

“Because we have zero business benefit to extending access to credit that is not repaid, we only approve consumers for what we believe they are able to repay,” Adkins wrote.

And that means the Affirm value proposition — that BNPL products can be better alternatives for judicious credit-building users — still holds. Affirm’s no-late-fees posture has helped American consumers save more than $300 million on fees while credit card debt and delinquencies continue to rise.

That’s because the interests of borrowers and lenders in the revolving-debt world of credit cards aren’t aligned, Adkins wrote. Because Affirm and other BNPL providers profit most from repeat business, they see to it that customers pay what they owe, positioning them for further success.

While the CFPB report raised valid questions about BNPL, it also validated key benefits of Affirm’s business model, according to Adkins.

“We’ve intentionally designed our products to prevent the debt traps that plague traditional credit cards,” she wrote. “We’re creating an environment where consumers are better positioned to succeed.”