Writer: Mike Senecal

Editor: Lillian Guevara-Castro

Reviewer: Adam West

Key Takeaways

- This week's third annual Vehicle Accessible Report from OpenLending reveals more near- and non-prime consumers are choosing used cars as ownership costs rise.

- Yet these consumers exhibit a higher propensity to purchase within the next two years than prime and super-prime consumers.

- Despite economic pressures, near- and non-prime buyers remain a resilient force in the auto market, with demand likely to fuel growth in used vehicle financing.

Everybody needs wheels — even this author, who was a fourth-grader at Holy Spirit School in Vacaville, California, when she published her pro-wheel opinion in 2015. So we perhaps should not be surprised that OpenLending’s third annual Vehicle Accessibility Report shows Americans are in the mood to buy new cars, even when they’re used.

That’s despite dramatically rising total ownership costs for both new and used vehicles, ballooning monthly payments, and longer loan terms. What’s happening is a kind of bifurcation in the market arising from credit score differences, OpenLending showed.

While prime and super-prime customers (described as those with self-reported credit scores above 700) still may feel the lure of that new-car smell, those with scores in the near- and non-prime range are increasingly opting for previously owned vehicles.

To reach that conclusion, OpenLending sourced pre-pandemic data to show that the preference for used cars in the near- and non-prime categories rose from 46% in 2017-19 to 56% in 2023-24.

OpenLending’s 2025 Vehicle Accessibility Report demonstrates the resilience of the subprime auto lending market.

Those consumers demonstrate slightly more interest in purchasing a vehicle, with 70% planning to acquire new wheels sometime in the next two years compared to 58% in the prime and super-prime categories.

Those numbers indicate that demand in subprime auto financing has legs. Near- and non-prime auto loan consumers give every indication they plan to continue pursuing vehicle ownership in the face of economic and cost challenges.

The December 2024 study surveyed 1,001 online respondents aged 18 and older, employing demographic quotas around age, credit score, and vehicle ownership status to derive a representative sample.

“Significant purchase intent exists among near- and non-prime and prime consumers, presenting significant market opportunities for lenders,” concluded OpenLending, a leading provider of AI and risk-based pricing for near-prime and non-prime auto loans. “By extending responsible auto loans to near- and non-prime borrowers, financial institutions can cultivate long-term customer relationships.”

Key Findings Emphasize Need for Responsible Auto Lending

The market opportunity for subprime auto lenders exists only to the extent they work to preserve it. By informing the lending community about consumer behaviors and market dynamics, the 2025 Vehicle Accessibility Report provides valuable insights to help lenders optimize their offerings to support sustainable loan growth and protect consumers from financial strain.

The report explains that near- and non-prime consumers are turning to used cars as that market undergoes a contraction, with the average day’s supply at 46 in 2025 compared to 55 in 2024. Consequently, the median monthly payment for subprime used car loans now stands at $400, up significantly since before the pandemic and by $100 since 2016.

Near- and non-prime borrowers measured in 2023-24 were also slightly less likely to provide a down payment than those measured in 2016 (55% to 58%). Depending on your point of view, there was good news for subprime borrowers in data reporting slightly fewer loans with terms of 72 months or longer in 2023-24 versus 2016.

OpenLending claims that the relative lack of longer-term loans for near- and non-prime borrowers increases the financial stress of vehicle ownership. Prime and super-prime borrowers, on the other hand, were significantly more likely to provide a down payment in 2023-24 and slightly more likely to elect for a 72-month or longer term.

Intuition tells me that some of the stresses in today’s market stem from the demand side, as consumers of all stripes opt for bigger cars and trucks and higher payments. Yet 61% of vehicle owners aspire to pay off their loans early, mainly because they feel it improves their future ability to upgrade.

To some extent, then, it’s a market of buyers who love cars and are willing to pay for them — or compromise their future over, as news articles on rising auto loan delinquencies attest. Still, 35% of those in the near- and non-prime category who don’t own a car indicate their chief sticking point is affordability. There’s room for cars and loans of all sizes.

“Rising prices and interest rates are deterring potential buyers,” the report noted.

Vital Consumer Intelligence in an Evolving Market

What drives subprime auto borrowers is that they get more out of the “personal” aspect of personal transportation than what they put in.

The report notes “greater access to employment opportunities and educational attainment,” which is valid. But I think people ultimately prefer to own their vehicles, as 82% in this report do, because of the wheels — meaning the freedom to travel beyond where your body can take you.

Sure, owning a car underscores the “vital role that vehicle ownership plays in supporting economic mobility and overall well-being in modern society,” as the report states. The miracle is that vehicle ownership can mean so many things to different people.

It’s an ambitious goal to measure the zeitgeist around something as basic as your personal set of wheels. OpenLending draws on its perspective as an industry leader to improve lenders’ understanding of near- and non-prime consumers, promote more inclusive auto financing practices, and help borrowers achieve greater financial stability.

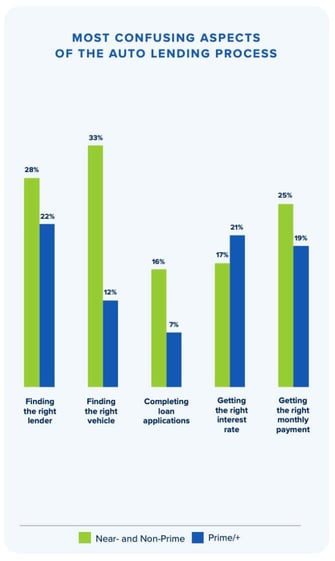

That doesn’t eliminate the need for improvement in all lending categories. For example, the survey found significant mistrust of bank, credit union, captive, and alternative auto lenders among near- and non-prime borrowers, including confusion about finding the right lender and vehicle and landing on the right monthly payment.

But as I mentioned before, the report also found respondents with upgrades on their minds embracing the prospect of moving more quickly into new wheels by paying off existing loans faster.

And everybody’s on the same page in favor of lower interest rates spurring action. A full 78% of near- and non-prime consumers, in fact, report lower rates as a significant purchase motivator.

Opportunities abound for all lending outlets to improve how they reach, educate, and convert consumers. Dealership financing teams remain the information outlet of choice for most, a reality OpenBanking considers an area in need of improvement.

But near- and non-prime is a growth market, the report concludes. We don’t know whether certainty around tariffs and inflation will cloud the demand picture moving forward. OpenLending helps us know consumers will buy if we let them.