Writer: Eric Bank

Editor: Lillian Guevara-Castro

Key Takeaways

New research from West Virginia University shows that what you do with your credit card today will set your financial course over your lifetime.

The study was authored by economists Scott Schuh and Scott Fulford and based on detailed credit bureau data to track borrowing and repayment patterns.

The study found that if you begin your credit journey with outstanding balances, you are highly likely to continue having them for decades. We’re talking about “revolving” use of credit, and it is distinct from paying off the total balance each month.

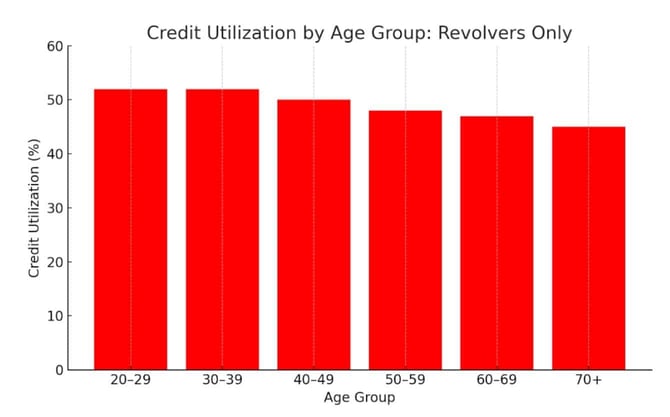

Credit utilization ratios — the amount of available credit cardholders use — also stay steady over time among credit cardholders, reflecting deeply entrenched financial patterns.

Moreover, this behavior doesn’t vary much with changes in a cardholder’s income or economic circumstances. “There is a lot of persistence,” Schuh told us. “If people start to revolve, they tend to stay there.”

Patience Can Sometimes Be More Significant Than Paychecks

You might expect that those with higher incomes would be more fiscally conservative. However, the WVU study found that individuals with good incomes and advanced degrees can still fall into long-term credit card debt.

So why is this? According to Schuh, the greatest distinction may boil down to something more difficult to quantify: patience.

The researchers separated consumers into two behavioral categories: patient (the payers) and impatient (the revolvers).

Patient consumers pay off their accounts each month and do not incur interest. Impatient consumers prefer to buy now and are more inclined to incur debt to do so, even if it costs them excessive interest charges in the long run.

“Impatience is found in places you would least expect,” said Schuh. “You see it with people of all income and education levels. It is not about how much you make.”

For those with poor credit, this will sound familiar. If you’ve struggled to get out of debt, you’ve likely had cycles of impulsive buying or borrowing just to get by.

The study doesn’t blame consumers for this. In fact, it theorizes that we are all wired this way. The question is how to break those patterns once they’ve been set.

What It Means for Impatient Spenders

Impatient consumers are not alone. The study indicates that these behaviors are ingrained habitual patterns and not easy to break. That said, awareness is a good place to start.

Consumers who are aware that they tend to spend without thinking can turn to tools that can keep them on track.

Software like Copilot or You Need a Budget offers visual warnings to inform consumers of overspending. Financial literacy can create better habits if introduced early on as well. While adult classes are useful in the short term, what is learned in high school is more long-lasting, Schuh found.

Ultimately, for consumers who struggle with revolving debt, this study shows it’s not just a matter of willpower. Their brains may be working against themselves. But with the right assistance and a plan, consumers can get themselves back on a positive track.

How Credit Reports and Policy Fail

The problem is that credit reports do not clarify whether consumers are paying interest on debt. That makes it tricky for researchers and lenders to know what is going on and who is having trouble.

For example, a consumer who pays their balance in full each month will look no different on a credit report than a consumer with a $5,000 balance who pays only the minimum. “That difference doesn’t register in the data,” said Schuh. “It should.”

The report also presented a provocative policy question: Instead of issuing stimulus checks in a downturn, what if the government asked lenders to expand credit lines?

That extra room for revolving consumers may encourage more buying. Unless those lines are reduced later on, though, Schuh warned that the long-term cost to consumers may be higher than the short-term benefit.

Methodology

Schuh and his co-author used anonymized credit bureau data on a large cross section of U.S. consumers and examined credit lines, balances, and utilization patterns over extended periods.

As credit reports do not reveal individuals who revolve debt, the researchers used statistical modeling to make inferences about behavior based on how individuals used and repaid credit.

This allowed them to trace patterns across decades and identify steady revolving patterns that would not be evident otherwise.