Is TransUnion Credit Score Accurate? FICO vs. VantageScore (Feb. 2024)

Written by: Ashley Fricker

Edited by: Lillian Guevara-Castro

There are so many credit scores out there nowadays that it’s easy to get confused as to which one is your “real,” or accurate, score. A TransUnion credit score simply means the score you’re viewing is based off your TransUnion credit report. But there are several credit score models, the most popular of which are FICO and VantageScore.

TransUnion will provide you with your VantageScore 3.0 credit score when you sign up for its credit monitoring service. VantageScore was created in partnership among all three credit bureaus — Experian, Equifax, and TransUnion.

Your TransUnion VantageScore is, in fact, accurate — based on the VantageScore model. This is where things get a bit tricky, but we’ll explain as simply as possible.

TransUnion is Accurate, But May Conflict With Other Scores

The only way your TransUnion credit score wouldn’t be accurate is if you found errors on your TransUnion credit report that are affecting your credit score. Unfortunately, errors can happen from time to time.

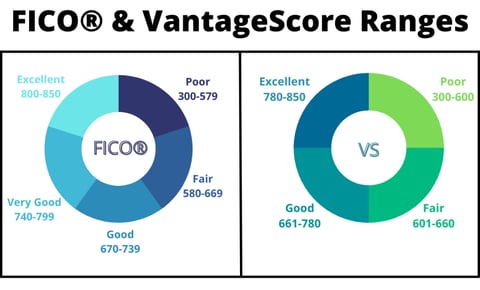

FICO and VantageScore both use a range of 300 to 850 to categorize credit scores. The scoring tiers that identify a consumer’s credit risk, i.e., “bad credit” are a bit different for each model, but generally close:

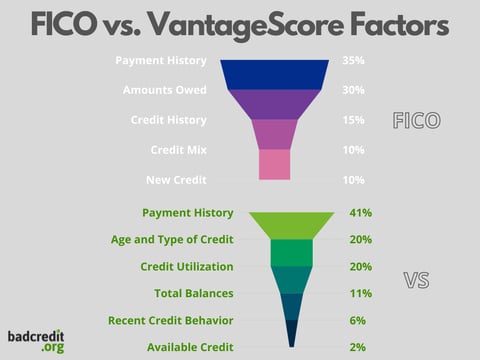

VantageScore also weights each credit scoring factor differently than FICO, as you can see below.

This graphic shows how VantageScore and FICO calculate scores differently.

Basically, you have FICO scores based on each credit bureau’s report, and you have VantageScores based on each report. You have dozens of credit scores that can vary based on numerous factors, but that doesn’t mean any of them are innaccurate.

Technically, credit scores are accurate according to wherever you get them from — unless there are errors on your credit reports that you need to dispute. If you do indeed have errors on your reports and don’t know where to turn for help, a credit repair service can walk you through the process.

Our top-rated credit repair service is Lexington Law, which offers a free consultation:

| |

- Since 2004, Lexington Law Firm clients saw over 81 million items removed from their credit reports

- Get started today with a free online credit report consultation

- Cancel anytime

- See official site, terms, and details »

| Better Business Bureau | See BBB Listing |

| In Business Since | 2004 |

| Monthly Cost | $99.95 |

| Reputation Score | 8/10 |

| Our Expert Review | 4.9/5.0 (see review) |

So, now that you know that your TransUnion credit score is likely accurate, the next plausible question is, Which score do lenders use?

FICO is the Most Widely-Used Credit Score By Lenders

Since there are so many free credit score resources out there, you should know that FICO is the most widely used credit score among lenders. In fact, 90% of lenders check FICO Scores rather than any other types of credit scores, though VantageScore is rapidly gaining popularity.

But if you’re looking to take out a loan anytime soon, we still recommend checking your FICO Score.

FICO actually has multiple scoring models, such as FICO Auto Score and FICO Bankcard Score, used in different lending industries. The most popular score across industries is the FICO Score 8, while the FICO Score 10 and FICO Score 10 T are the most recently released FICO scoring models.

You can purchase your FICO credit score and report from each credit bureau individually for $19.95 or all three credit bureaus scores and reports for $59.85. Purchasing your credit score through FICO will include your FICO Score 8, as well as other important industry-specific scores, which is much more than you’ll get from a free service.

Credit scoring has gotten unnecessarily complicated over the years, but countless companies are dedicated to demystifying credit for regular people who don’t write about finances all day, ahem.

These companies, most notably Credit Karma, can show you your VantageScore credit scores as well as recommendations for improving your credit in an easy-to-read format. But it will also use your data to recommend products and services based on your credit profile, which may or may not be something you want.

The Bottom Line

Your credit scores are only incorrect if the credit report from which it is based has errors — but know that credit reports are correct an overwhelming majority of the time.

You can review your credit reports — one from each bureau — for free every year on AnnualCreditReport.com. It is the only federally authorized source to provide you with your full credit report. Everything you see on a personal finance app or the like is a credit report summary.

Advertiser Disclosure

BadCredit.org is a free online resource that offers valuable content and comparison services to users. To keep this resource 100% free for users, we receive advertising compensation from the financial products listed on this page. Along with key review factors, this compensation may impact how and where products appear on the page (including, for example, the order in which they appear). BadCredit.org does not include listings for all financial products.

Our Editorial Review Policy

Our site is committed to publishing independent, accurate content guided by strict editorial guidelines. Before articles and reviews are published on our site, they undergo a thorough review process performed by a team of independent editors and subject-matter experts to ensure the content’s accuracy, timeliness, and impartiality. Our editorial team is separate and independent of our site’s advertisers, and the opinions they express on our site are their own. To read more about our team members and their editorial backgrounds, please visit our site’s About page.

")

")

")